Clear principles needed for debt relief program

Clear principles needed for debt relief program

Posted July. 22, 2022 08:03,

Updated July. 22, 2022 08:03

The presidential office announced on Tuesday that the debt relief program that slashes the interest payment for young debtors to a maximum half is “not designed to write off the principal, but to extend the deadline for servicing debt and lower the interest rates in certain cases.” Kim Joo-hyeon, the head of the Financial Services Commission, even implored to “understand the purpose of this program with a warm heart.” The announcements came after the spread of controversies over the backlash against the debt restructuring for youth, labeling it as a bailout for heavily indebted investors.

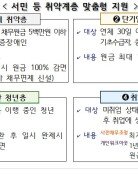

The Financial Services Commission issued a plan on July 14 to alleviate the financial trouble for ordinary folks, offering reduction of interest, postponement of principal repayment, and application of lower interest during the postponement period for 48,000 young debtors with lower credit ratings. Those who posted losses in cryptocurrency investments are also eligible.

The existing debt restructuring only offers an extension of repayment without cancellation of interest payments, and its agreed annual interest rate is also relatively high at a maximum 15 percent. The government argues that the newly introduced debt relief program has only expanded its scope towards youth population with lower credit ratings, but it is evident that the new program offers far more extensive benefits to debtors.

Of the 1,860 trillion won in household debt, 597 trillion won was from heavy debtors who borrowed money from multiple financial companies. The financial authorities must check the exact status of vulnerable households on the verge of bankruptcy before the bomb of debt explodes. The right order of business must start by setting a longer-term plan to induce repayment and liquidate distressed debts if repayment is not viable. Yet, they skipped those due processes to propose a pork barrel program canceling interest payment and principal repayment for the young and the self-employed, respectively. Owing to this controversial decision, the prerequisite restructuring of liabilities is facing trouble.

Be it younger investors or the self-employed, it is deceptive to support them when most of the debtors are fulfilling their duties for debt servicing. Above all, cutting interest or cancelling debt arbitrarily can lead to banking failures. It might be the owners of smaller businesses that have to bear the brunt as their request for urgent loans can be rejected as distressed debts can erode the credit capacity of financial institutions. Supporting debtors without drawing a line between speculators and ordinary debtors might lead to squandering the coffers of the government.